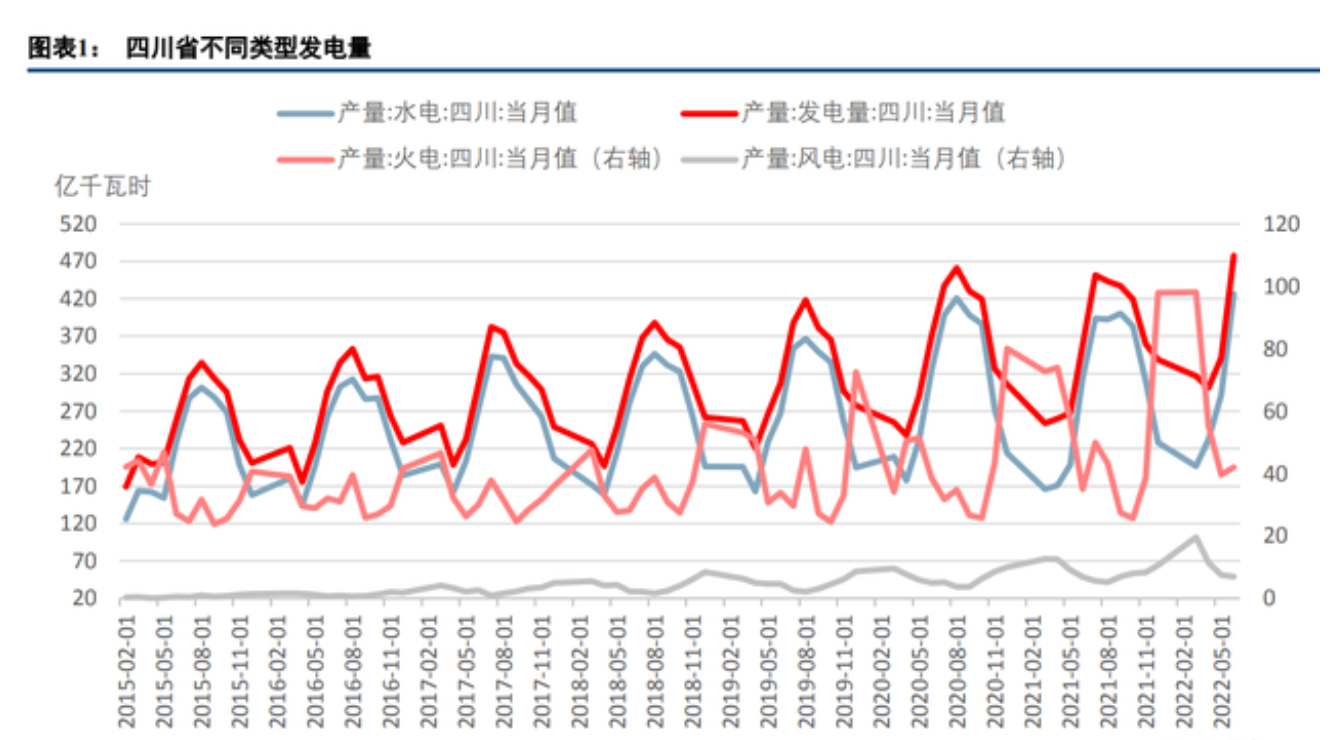

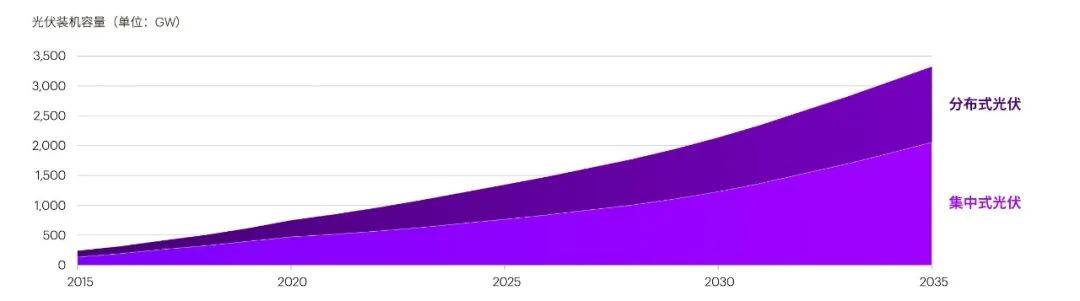

Since July, the high temperature weather across the country has continued to intensify, and parallel to the high temperature is the continuous record-high power load level. At the same time, my country's water supply has changed from abundant to dry, the hydropower output capacity of my country's second largest power source has weakened year-on-year, and the peak pressure of thermal power has increased significantly year-on-year. Recently, Sichuan Province issued a document to implement a high temperature holiday to allow electricity to be used by the people; some areas have also received notices of power cuts since the beginning of this month. Under the background of power shortage, on the one hand, traditional energy sources such as coal benefit from supply constraints and demand boom. Extremely high temperature weather has led to a cooling load of nearly 18 million kilowatts of air conditioners in Sichuan, and the largest electricity load in Sichuan province may reach 60 million kilowatts, an increase of 25% over the same period last year. On the power supply side, the installed power capacity in Sichuan Province is dominated by hydropower and supplemented by thermal power. In June 2022, the installed capacity in Sichuan Province will reach 109.01 million kilowatts, of which hydropower is 88.44 million kilowatts, accounting for 81.1%, and thermal power is 18 million kilowatts, accounting for 16.5%. Overall power generation is highly dependent on hydropower. In Sichuan, the inflow of hydropower was 40% dry in July. Since August, the inflow of hydropower has been dry by 50%. The water storage of reservoirs and hydropower stations is seriously insufficient, and the hydropower generation capacity of the province has dropped by more than 50%. Recently, the power sector including coal, photovoltaics, nuclear power, and wind power has collectively risen sharply and has gone out of the independent market. Although the electricity consumption situation in some areas is tense, at present, there may not be a large-scale "switching off" phenomenon, but the "tight balance" of power supply and demand will continue in the future. Under the "tight balance" of power supply and demand, thermal power, as a stable and regulated power source, still plays an important role in ensuring power supply in the entire power transformation process. In addition, with the improvement of the economy of new energy sources such as photovoltaics, and the promotion of energy conservation and emission reduction policies in various countries, related industries are expected to continue to boom. |Energy structure transformation intensifies Under the global trend of "carbon neutrality", the power generation industry, as one of the important carbon emission industries, is facing the rapid increase in the proportion of renewable energy, the rapid growth of distributed energy, the significant improvement in energy utilization efficiency, and the more diverse consumer demands. aspects of changes. Compared with the low-carbon transformation trend of the global power industry, China's power industry is also experiencing the trend of distributed power generation gradually replacing centralized power generation, new energy power generation gradually replacing traditional energy power generation, and terminal energy power replacing traditional energy use. It is estimated that by 2035, the proportion of global coal power will drop to 24%, and the renewable energy power generation will reach 17,443TWh, accounting for more than half of the total, with an average annual growth rate of 6%. In the future, the form of energy supply will also change, among which distributed energy will become one of the main growth points. In the first half of this year, domestic distributed demand and overseas demand exceeded market expectations. According to the National Energy Administration (data), the domestic 2022H1 photovoltaic installed capacity was 30.88GW, an increase of 137.4%, and the installed capacity continued to exceed market expectations. In the second half of the year, the large domestic bases will increase the volume, and centralized photovoltaics may become the point of exceeding expectations in the second half of the year, and the newly installed capacity may reach more than 100GW throughout the year. The European energy crisis has accelerated the transition to clean energy, and the anti-avoidance dust has settled, and the demand for modules in the United States is expected to improve significantly in the second half of the year. The penetration rate of new technologies such as supply-side N-type batteries has increased. At present, TOPCon batteries are already economical and are also the focus of the market. It is estimated that by 2030, distributed wind power will provide at least 30GW of energy for the United States, and China is gradually promoting small and medium-sized distributed wind power to islands, lakes and other regions. In terms of distributed photovoltaics, the installed capacity of global distributed photovoltaics will increase from 146GW in 2017 to 1,264GW in 2035, accounting for 38%. |The power industry chain ushered in multiple opportunities At present, the high temperature has further led to an increase in power demand, resulting in a shortage of power supply in some areas. In the short term, thermal power and nuclear power are expected to benefit from supply guarantees. In the long run, extreme weather is frequent, and coal demand is expected to improve. Distributed photovoltaics, cross-regional and distributed distribution network systems are expected to accelerate construction to ensure energy security. From the perspective of electric power construction, the State Grid recently announced that it will fully promote the construction of major projects, and the investment in the power grid has continuously exceeded expectations. Data shows that from January to July this year, the State Grid completed grid investment of 236.4 billion yuan, a year-on-year increase of 19%. Currently, the total investment in projects under construction is 883.2 billion yuan, and nearly 300 billion yuan will be completed by the end of the year. The total investment in projects under construction is expected to be A record high of 1.3 trillion yuan. Since the beginning of this year, stable growth has become an important theme, and grid investment projects are expected to continue to increase. The construction of a new power system with new energy as the main body has put forward higher requirements for the grid. According to the action plan for the two networks, UHV and distribution network intelligence have become the focus of construction. In the early stage, the investment schedule was delayed due to the disturbance of the epidemic. With the implementation of the stable growth policy, the follow-up planning projects are expected to be implemented quickly, and the power industry chain will usher in multiple opportunities. The following three sub-areas: 1. Virtual power plant Virtual power plants are one of the most economical options for addressing peak loads on the grid. With global temperature rise and rapid economic development, peak loads are high and short-lived. In order to ensure more economical power supply and avoid power outages, demand-side response has received widespread attention. The development of domestic virtual power plants is still in the initial stage, and there is a broad space in the future. 2. UHV State Grid previously stated that it will start construction of a new batch of UHV projects in the second half of the year, with a total investment of over 150 billion yuan. The industry believes that there are high technical barriers in the UHV equipment segment with a better competitive landscape, and the performance of related equipment suppliers may usher in a peak next year and the next year. 3. Smart grid In the context of the "dual carbon" goal, changes in my country's energy structure have led to a series of problems such as insufficient power grid capacity, mismatch between power generation and power consumption, and decline in the complete stability of the power grid. In order to solve these problems, increasing the construction of smart grid has become an important part of the current grid construction. In the short and medium term, due to the failure to anticipate the impact of extreme weather and insufficient preparations, the only way to deal with it is staggered production or power outages, which cause some troubles to the stability of the supply chain and economic development. In the long run, it is recommended that investors look for investment opportunities from the following three aspects: first, the source side, focusing on the incremental development opportunities of the new energy + energy storage industry chain; Development opportunities; the third is the mechanism side, focusing on the reshaping opportunities of the energy operation business model under the reform of the electricity market and carbon market.