On Friday, March 28, the U.S. Department of Commerce released data showing that the core PCE price index, the Fed's favorite inflation gauge, rose 2.79% year-on-year in February, the highest since December 2024.

As the Fed's most concerned inflation indicator, the market generally expects upward pressure on the PCE in February under the influence of firm core services prices, which will further affect the Fed's subsequent interest rate cut prospects.

If the February PCE data continues to cool down, it may raise the market's interest rate cut expectations marginally, but if the PCE data heats up more than expected, it may reduce the market's bets on the Fed to cut interest rates in the near term, which in turn will have an impact on the trend of US stocks, the US dollar and gold.

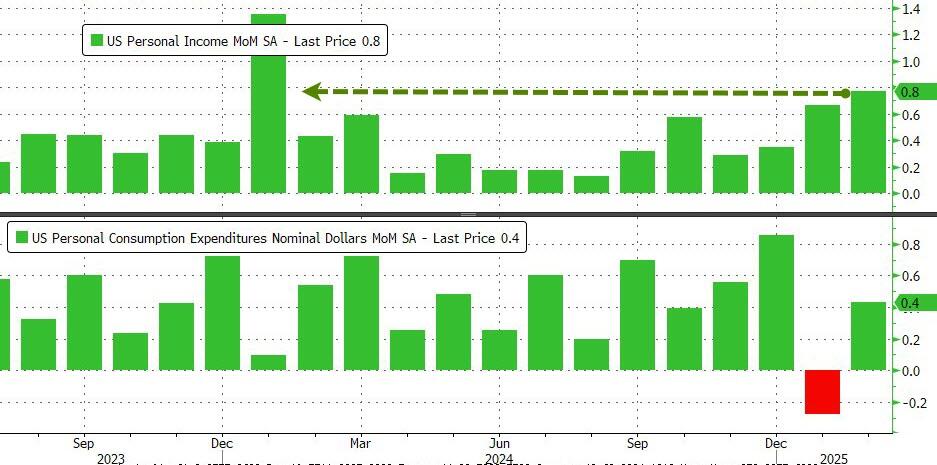

Consumer spending slowed and the savings rate rose further

Personal consumption expenditures (PCE) rose 0.4% month-on-month in February, while inflation-adjusted personal consumption expenditures edged up 0.1% month-on-month, after falling 0.5% in January, the biggest decline in nearly four years, which economists blamed on bad weather.

As prices rose, so did personal income, rising 0.8% month-on-month, the largest increase since January 2024 and outpacing the 0.4% increase in personal spending.

The gap between income and spending has pushed the savings rate to its highest level since June 2024, suggesting that consumers are more cautious about their finances. Other signs suggest that Americans are under greater financial pressure, including delinquent car payments and difficulty raising emergency funds.

Inflation remains the Fed's focus

Inflation remains one of the core contradictions of the US economy. The Fed's latest economic projections at the March FOMC meeting revised the median 2025 PCE and core PCE inflation forecasts upwards by 0.2 and 0.3 percentage points to 2.7% and 2.8%, respectively, still significantly above the 2% policy target.

The word Powell emphasized the most at the meeting was "uncertainty", and he believed that most of the variables in the US economic outlook come from the back-and-forth of tariff policy.

Research firm Inflation Insights Inc. (Inflation Insights) founder Omair Sherif (Omair Sharif said the market is inclined to "skip" the February PCE report and think about the impact of tariffs on future inflation. Therefore, if the data rises more than expected, it will further exacerbate the market's anxiety about rising inflation in the long term and the US economy falling into "stagflation".

President of the Federal Reserve of Boston, 2025 FOMC member Susan Collins said on the 27th that Trump's tariffs will push up U.S. inflation, and it is unclear how long this upward pressure will last.

Collins said that due to the upside risks of inflation and the pressure on the economy from various uncertainties, the Fed should keep interest rates stable for a long time, and the Fed should continue to be patient and ready to respond flexibly in the future.

Jingtai believes that inflation in the United States will be a persistent and recurring topic this year. From the macro background, it is an objective reality that trade and supply chains will continue to be disrupted by U.S. policies in the coming period, so it is a high probability event that the inflation center will remain high.

In addition to that, for this year, the different components have different drivers. To put it simply, U.S. inflation is like a "small power that can't be killed", and it will be tossed again and again this year. Investors need to fasten their seatbelts and be prepared for possible market fluctuations. After all, in the face of inflation, it is better to prevent it in advance than to remediate it after the fact.

How does the market react?

While the PCE (Personal Consumption Expenditures) cooled in February, and while this sounds like good news, it may not actually ease the market's concerns about rising prices.

If the PCE is only a temporary decline, then investors' expectations of a rate cut will put pressure on the dollar. Conversely, if PCE unexpectedly recovers, risk aversion will rise again.

This is not a good thing for US stocks, which could be further pressured. Especially in the current situation of high interest rates coupled with low growth, the valuation model of equities will be adjusted, which means that the present value of future earnings becomes lower, which puts downward pressure on stock prices.

In the current economic environment, Jingtai believes that gold may be the "paradigm answer" to asset selection. During periods of "stagflation" like the two typical ones in US history (1974-1975 and 1979-1982), gold performed very well, especially in the first year of stagflation. As U.S. stocks have become more volatile this year, gold seems to be a more attractive asset option.

In addition, the holdings of SPDR, the world's largest gold ETF, have been increasing since the beginning of the year, and it seems that the bulls are gradually gaining the upper hand in the game against the bears. In short, in this period of uncertainty, gold could be an "airbag" in asset allocation. After all, when the market is groping in the inflation maze, it is always wrong to hold some "hard currency".